FX Execution Timing: Why When You Trade Matters

OPTIMIZING FX EXECUTION FOR CORPORATIONS · PART ONE

How the time of day and the fixing windows move the cost of FX execution

For corporate treasury teams, the conversation about FX cost usually centers on the spread a bank quotes. There is a second lever that is just as real and far less discussed: when in the global day a trade is executed. The same currency, in the same size, can cost materially more at one hour than another, because liquidity (and dealers’ willingness to price tightly) moves continuously around the clock. This paper looks at how that intraday pattern works, why the busy fixing windows are not the cheap ones, and two simple timing rules that follow.

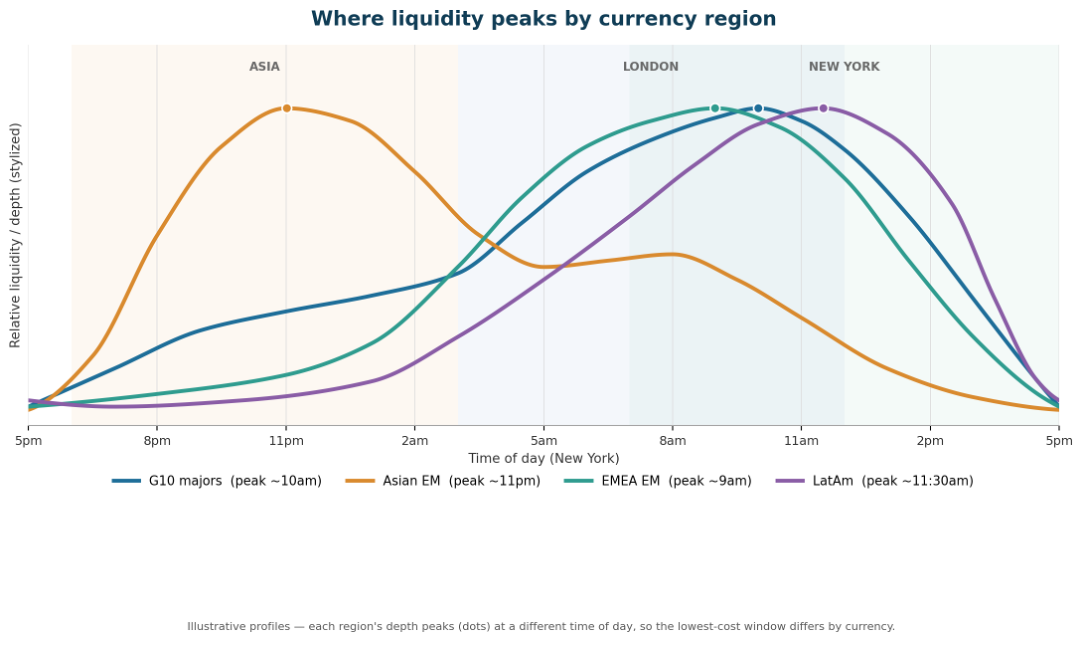

Liquidity moves around the clock

FX liquidity is deep, but it is not spread evenly through the day. Each currency is deepest during its own home session and thinnest when that market is closed. The chart below sketches the pattern for four broad groups, all on a single New York-time axis.

Three things follow. The major currencies are deepest in the London – New York overlap, late morning New York time. Emerging-market currencies peak in their own region: Asian names overnight in New York hours, EMEA names through the European morning, Latin American names around the New York midday. And because the peaks fall at different times, the cheapest moment to trade is currency-specific: a window that is ideal for the euro can be the thinnest, most expensive part of the day for the rand or the won.

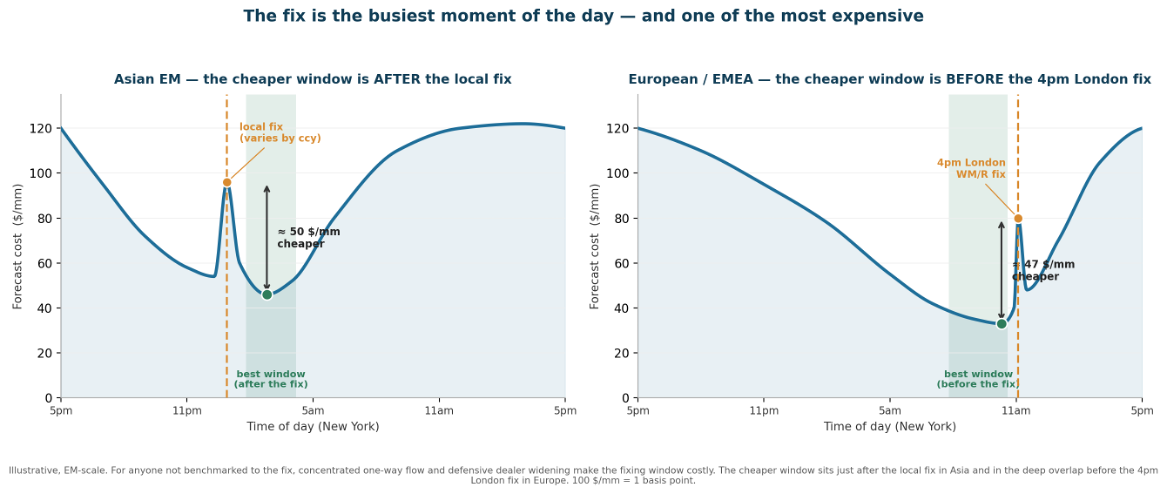

The fix is the busiest moment, not the cheapest

Every trading day has reference “fixing” windows, most prominently the 4pm London WM/R fix, alongside local fixings in each market. These are the highest volume moments of the day, which can make them feel like the safest time to trade. For most corporates the opposite is true. Around a fix, flow is concentrated and largely one-directional: many participants rebalancing the same way at the same instant. Dealers widen their prices defensively to avoid being run over. Unless a company is specifically benchmarked to the fix, executing into it usually means paying for that congestion rather than benefiting from it.

Two timing rules that follow

The practical implication differs by region, and the two point in opposite directions around the fix:

- Asian currencies: trade after the local fix. The fixing-related flow clears shortly after the local fix; liquidity is typically deepest, and spreads tightest, in the window just afterwards.

- European currencies: trade before the 4pm London fix. The deepest liquidity of the European day sits in the late-morning London – New York overlap, ahead of the fix; once the fix passes, European depth begins to fade.

What it can be worth

The size of the prize depends on the currency and the trade. As rough, illustrative orders of magnitude (100 $/mm = 1 basis point):

- Major currencies. Steering around the thinnest windows is typically worth roughly 10-20 $/mm (about 0.1-0.2 of a basis point).

- Emerging-market currencies. Trading in the home session rather than the overnight lull is commonly worth 50-150 $/mm (around 0.5 basis point to more than 1).

- Around the fix. For a non-benchmarked trade, the after-the-fix window in Asia and the before-the-fix overlap in Europe each tend to run on the order of 40-50 $/mm cheaper than executing into the fix (the gap can be wider on heavily directional fixing days).

One caveat matters: these are gross figures. Waiting for a better window carries its own risk: the market can move against you in the meantime. The right comparison is always the expected saving net of that timing risk, which is larger for patient, low-urgency flow and smaller for urgent trades in volatile conditions. And cumulatively, you would get better results over many trades.

Key takeaways

- Time of day is one of the largest, least-discussed drivers of FX execution cost.

- The cheapest window is currency-specific: there is no single “best time to trade.”

- The fix is the busiest window, not the cheapest, for anyone not benchmarked to it.

- Rule of thumb: trade Asian currencies after the local fix, European currencies before the 4pm London fix.

- Always weigh the expected saving against the risk of waiting.

Execution timing can meaningfully impact FX costs, but it is only one factor in a comprehensive FX risk management strategy. Learn how BankMinder helps treasury teams measure execution quality, analyze transaction costs and evaluate bank performance. To see how these capabilities fit into a complete FX risk management platform, explore the AtlasFX Overview page.

In Part Two of Optimizing FX Execution for Corporations, we will look at trade sizes; in Part Three, we will focus on choosing the bank panel.

Illustrative figures throughout; actual costs vary by currency, trade size, and prevailing market conditions. 100 $/mm = 1 basis point. Informational only — not investment advice.